Three years after interest rates peaked, the gap between supply and demand in European student housing and self-storage is wider than ever. Demand, anchored in demographic need, did not contract. The growth in supply slowed. Understanding why the gap will not now correct requires an understanding of the key factors on both sides.

When capital allocators look at European operational real estate today, the familiar narrative runs: strong demand, constrained supply, a persistent gap. The mechanisms producing it are self-reinforcing on both sides, and the standard remedies (more capital, faster planning, lower rates) do not reach the root cause of either.

The rate correction of alternative real estate investments in 2022-2024 revealed this asymmetry in stark terms. Student enrolments continued rising. Self-storage usage, driven by urban densification and housing mobility rather than consumer confidence, held firm. Supply did not. New PBSA completions fell 39% in 2024-25. Residential completions across Europe fell 11% in 2024, with further falls recorded through 2026.

Demand: Two Structural Engines

The headline case for European PBSA is well rehearsed: international student numbers are growing, European universities are competing for a larger global student population, and provision has not kept pace. JLL estimates a current shortfall of over 3 million beds across Europe, independently corroborated by Savills at 3.1 million.. Development constraints will keep completions 79% below the number of new student arrivals over the next five years. Where supply has been delivered, the market has responded. Private PBSA across Continental Europe generated 9% rental growth in 2025-26 against inflation of 2.1%, with occupancy at 96% for the year.

The less-discussed argument concerns domestic students. Across Southern Europe today, approximately half of domestic students live at home during university. Conventional demand analysis reads this as preference. The occupancy evidence reads it differently: where the product has been built, domestic students take it. The pattern holds either way - where managed PBSA has existed, demand has shown up; where it has not, demand has had no means of expression.

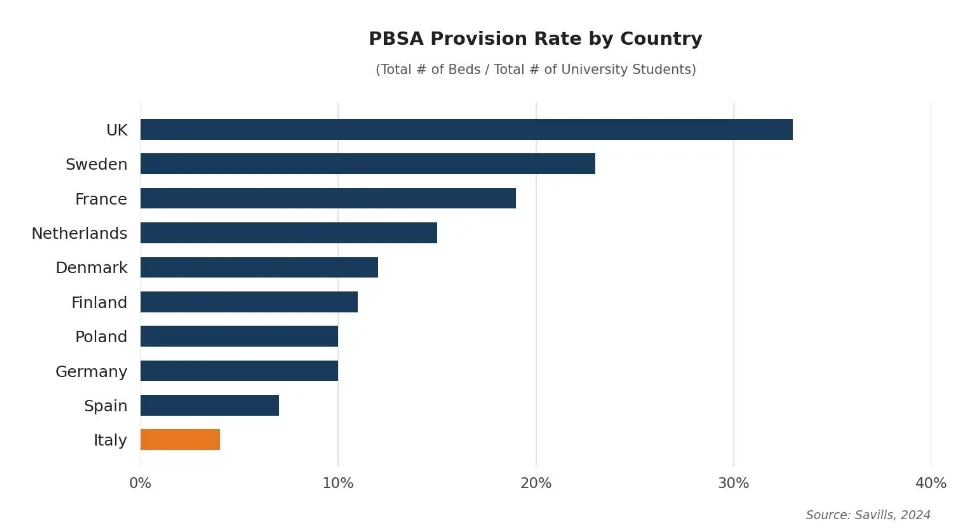

Italy illustrates the point most sharply. Its PBSA provision rate is around 4% - the lowest in Europe, against an EU average of 15% and a UK benchmark of 33%. City-level shortfalls are extreme: Bologna records a 13:1 demand-to-supply ratio; Rome 12:1. The Italian government committed €1.2 billion of PNRR funding to deliver 100,000 student beds by 2026. Even with that injection, significant undersupply persists. When state intervention at that scale does not close the gap, the structural depth of the problem is evident.

The UK's trajectory is instructive. Provision there now sits at 33%. It did not begin there. The shift from low provision toward that figure occurred as supply was built and domestic demand (previously unserved) emerged to fill it. Southern European markets have a destination; the question is the pace of travel, and that is a function of supply.

The student who occupies PBSA at 19 is, increasingly, the long-term urban renter at 35. The affordability conditions that make managed student accommodation the most viable option in university cities do not abate in the years that follow. That same cohort, in a different phase of life, is the structural foundation of the self-storage opportunity.

Self-storage demand in Europe is conventionally framed around life events: the three Ds of death, divorce and downsizing. Each produces a storage customer triggered by circumstance, with a median tenure of around two years.. That demand is real and durable, but an incomplete description of the current European market.

A structural second driver is emerging from Europe's housing affordability crisis. Home ownership among 25-39 year olds across Europe has declined from above 40% before 2013 to approximately 27%, and the conditions since have continued in one direction. EU house prices have risen more than 55% since 2010 while wages have not kept pace. Over a quarter of 18-34 year olds across Europe now spend more than 40% of disposable income on housing: the EU threshold for severe cost overburden. In some urban markets, the proportion of average wages required to rent a starter home reaches 60-70%.

Self-storage demand is concentrated at two ends of the customer spectrum. At one end, the event-driven 3D customer: a transactional need, short-lived but recurring reliably across the population. At the other, the chronic renter for whom storage has become a fixed cost of urban living rather than a response to a transition - lower churn, longer tenure, demand that does not diminish when economic conditions improve. Operators with the flexibility to serve both ends of that spectrum are adapting their format mix accordingly - city-centre, smaller-format units positioned not as a separate product but as the same need expressed at a different scale.

Continental Europe's self-storage penetration rate of approximately 0.03 m² per capita against 0.09 m² in the UK and 0.65 m² in the US reflects both the relative youth of the market and the scale of headroom available.. Both ends of the demand barbell are growing simultaneously. The gap between where penetration currently sits and where demographic and housing shifts are carrying it is the investment case.

The Supply Constraint Most Analysis Has Not Named

The conventional explanation for why supply cannot close the gap runs as follows: planning systems are slow, construction costs are elevated, and development finance retreated when rates rose. Each is accurate, but none is the most important constraint currently in place.

The European construction workforce is in structural demographic decline. The European Construction Industry Federation estimates a deficit of 2.1 million construction workers across EU member states in 2026, a figure that has grown every year since 2020 and shows no sign of reversing. The construction sector job vacancy rate in Q1 2025 was 2.9%, the highest of any EU sector, exceeding both services at 2.5% and industry at 1.6%. The average age of a European construction worker is now 44. In Spain the figure has risen from 37 in 2007 to over 45 today, at almost double the ageing rate of the broader economy, with only 16% of construction workers under 34. Vocational training enrolment is declining across Western Europe simultaneously. EU construction employment fell by 230,000 between 2010 and 2023.

This is not a cyclical shortage that recovers with the order book. It is a structural demographic problem. Euroconstruct's Q4 2025 survey found that 68% of German construction firms, 71% of Austrian and 65% of Irish cited labour availability as the primary constraint on order fulfilment - above materials costs and above permitting delays.. The pipeline of trained replacements does not exist at the required scale.

The implication for supply is direct. Even in a world where planning reform accelerated and financing became freely available tomorrow, the physical capacity to deliver new PBSA at the volume the gap requires does not exist. The constraint does not, however, apply equally to those already operating within the market. For operators with existing assets and local capability, it is not a barrier to supply. It is a barrier to competition. There is, however, one supply route for which the ground-up workforce constraint does not apply with equal force, and it is the route that works with the existing built stock rather than against the construction pipeline.

Why Capital Alone Does Not Solve This

There is a rational counterpoint that sophisticated allocators will raise: if the gap is as large and as durable as this argument suggests, why does capital not simply flow in and close it? Capital is not the binding constraint, and has not been for some time.

Planning permission cannot be bought. Across European urban markets, the pathway from land acquisition to occupied accommodation runs to five years or more under normal conditions. The EU launched the European Strategy for Housing Construction in December 2025 specifically to address the permitting and digitalisation barriers slowing delivery, a signal not of imminent resolution but of how deeply embedded the problem is.

Operational capability cannot be transferred quickly. The accommodation decision for a student arriving in Milan or Bologna is not made in a spreadsheet. It is made on the basis of location, quality and reputation, built over years of operating in a specific market. Managing a PBSA portfolio in Italy requires on-the-ground expertise in local regulatory compliance, lease-up dynamics, pricing strategy and brand positioning that is not replicable on a deal timeline. Self-storage follows the same logic. In markets where consumer awareness is still forming, what separates margin-competitive operators from those who fill slowly and price reactively is catchment analysis, dynamic pricing capability and digital acquisition - skills that take years to build and cannot be imported when a yield becomes attractive.. These barriers do not dissolve when yields improve. They advantage those who built that capability before the opportunity became visible - and that is the quality worth identifying in any operating partner.

Conversion: The Supply Strategy the Market Has Selected

There is one route where the conventional constraints do not apply with equal force. Europe is simultaneously oversupplied with the wrong kind of real estate. Secondary office vacancy across major markets remains structurally elevated, with the continent estimated to be 10-15% oversupplied with offices, many of them effectively obsolete. AEW data shows that office conversions represented over 30% of total European office transactions in the first four months of 2025, up from 17% in 2024 and 8% at the post-financial-crisis average.

Conversion bypasses the most labour-intensive phases of ground-up delivery, compresses the pathway from acquisition to income-generating operation from three to five years to twelve to eighteen months, and moves through planning on faster timelines, capturing the current rental growth window that a new-build pipeline cannot access.

In Italy, the legislative environment has moved to accelerate this directly. Decree-Law 19/2024 (DL PNRR 4) introduced a simplified procedure for converting existing properties to university residences, permitting the change of use as an explicit derogation from local zoning requirements, removing the municipal plan barrier that would otherwise block many urban conversion opportunities. A subsequent decree, DL 160/2024, replaced the requirement for a full building permit with a self-certified commencement notice (SCIA), materially shortening approval timelines.. The practical result: Milan recorded 38 office-to-student-housing change-of-use projects in 2025 alone. The mechanism is active and being used at scale in the cities where undersupply is most acute.

France has adopted parallel legislation allowing mayors to override local planning rules for office-to-university residence conversions.. The regulatory tailwind for conversion is now multi-jurisdictional. Governments that have recognised the political cost of the undersupply are lowering the planning barrier to the supply route most compatible with the workforce constraint (conversion), while leaving the barrier to ground-up unchanged.

For operators with the expertise to identify, acquire and reposition existing structures, the new-build bottleneck does not determine the supply equation. Conversion is not a workaround. It is the supply strategy most aligned with the structural conditions the market has produced.

What the Gap Looks Like

In student housing, the shortfall is measurable, growing and investment-grade. JLL's 3 million bed estimate is corroborated independently by Savills at 3.1 million. Completions will run 79% below new student arrivals for the next five years. Continental European private PBSA has been operating at or near capacity. PBSA investment across Europe grew 52% in 2025, with Continental European volumes exceeding the UK for the first time, a structural re-rating that has not yet closed the gap between capital interest and available quality stock.

Italy sits at the most acute end of this spectrum. A 4% provision rate, city-level demand ratios of 12:1 to 13:1, and a legislative framework now explicitly designed to accelerate conversion-led delivery combine to produce a market where the structural gap is the largest in Europe and the execution pathway (for an operator already on the ground) is more legible than at any point previously. The provision rate analysis is certainly a crude measure as students must live “somewhere” prior to the construction of PBSA - either at home or in private rental accommodation, however, to say it is an irrelevant metric is equally crude. Where PBSA exists, there is undeniably strong demand for it, with less price sensitivity from international students who prefer to pay a single bill for their accommodation and utilities rather than team-up with relative strangers to navigate the local bureaucracy that inevitably comes with renting. There is also an incentive for governments to be a proponent of PBSA as it frees-up the private rental sector for young professionals who are in desperate need of affordable housing in urban centres.

In self-storage, the gap is structural and less visible, which makes it more durable. Customers who have never used self-storage do not appear in vacancy statistics. What does appear is the performance of well-managed facilities in established demand pockets is 5.4% annual rental rate growth across Europe, 70% of operators expecting further occupancy and rate improvement in the next twelve months, and record investment volumes of €1.2 billion across UK and European markets in 2024. Markets where consumer awareness is growing fastest (Germany, Spain, Portugal) are recording the strongest rental growth.

The structural argument is about the convergence of two demand pools (event-driven and chronic) in markets that are still at a fraction of the penetration levels recorded in more mature storage economies.

Where This Leaves Capital

European student housing and self-storage are structurally undersupplied because the forces generating demand and the forces constraining supply have moved in opposite directions for years, and both movements are now accelerating rather than stabilising. Demand grows with demographics and compounds as housing unaffordability creates a generation of long-term renters with undersized accommodation and no near-term exit from that position. Supply is constrained by planning systems that pre-date the current demand profile, by construction economics that remain difficult for marginal development, and by a workforce that is ageing out of the industry without a sufficient replacement pipeline.

The standard investment narrative frames this as a gap to be closed. The more precise framing is that it is a condition being maintained by structural forces on both sides that are unlikely to resolve within a single investment horizon. That durability is the vintage argument: capital entering now is not anticipating a gap that will close behind it but locking in exposure to a condition that is more likely to deepen than resolve within the investment period.

The investment question is not whether the opportunity is real. The evidence on that is unambiguous. It is whether the capital entering the market arrives with the local knowledge, the operational depth and the execution capability that the opportunity demands, and whether the strategy is built around the supply route that structural conditions have selected. The gap rewards those already positioned at the pressure points where structural shortfalls are converted into durable income. The question is whether the operating partner has been built for these conditions, or for conditions that no longer exist.

Crosswind Capital Fund Management Limited is registered in the Abu Dhabi Global Market and regulated by the Financial Services Regulatory Authority (FSP: 220171). This article is for informational purposes only and does not constitute investment advice or a solicitation to invest.