The adjustment is over. European real estate has repriced, bid-ask spreads have closed, and capital that sat on the sidelines through 2023 and 2024 is now asking the same question it always asks too late: when does recovery begin? That framing is wrong, and the investors relying on it are waiting for something that will not arrive. The market has not been through a period of underperformance. It has been through a correction that was, by any rational measure, overdue. As pricing stabilises and opportunities emerge across both traditional holdings and alternative real estate investments, the focus should shift from predicting a recovery to identifying where value is being created. For capital sitting on the sidelines, it is the only question that matters. It determines whether you are buying into the right assets at the right moment, or standing aside while someone else does.

European direct real estate capital values fell roughly 19% from their June 2022 peak, according to MSCI data. Germany and France each recorded their worst quarterly returns on record in late 2022, worse than the drawdowns of the global financial crisis. The narrative that settled around those numbers described a sector that had underperformed: overvalued, overleveraged, caught out by a rate environment it had not anticipated. That narrative is not just wrong. It is asking the wrong question. Assets do not underperform in isolation. They underperform relative to a benchmark. And the benchmark against which European real estate has been measured for the past three years was itself the product of a monetary experiment so unusual that using it as a yardstick for anything is an analytical error.

The distinction between underperformance and mispricing matters. Underperformance implies mean reversion: wait long enough and things normalise. Mispricing implies something structural. Assets were priced on assumptions that no longer hold, and the correction was not a malfunction. It was the market doing exactly what it should. The question for allocators in 2026 is not when recovery begins. It is whether assets now sitting at corrected prices, particularly those whose income fundamentals were never impaired, are priced for the world as it is rather than the world as it was.

Ten Years of Free Money, and What It Actually Bought

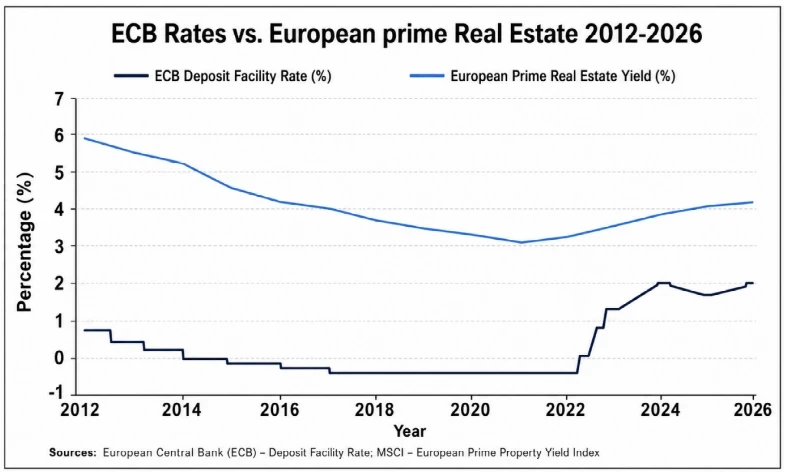

From 2012 to 2022, the ECB held its deposit rate at or below zero. For much of that period, German ten-year Bunds offered negative nominal yields. Investors allocating to European sovereign bonds were, in real terms, paying for the privilege of holding them. Capital that required positive returns had nowhere to go except into assets with income, and real estate, with its visible yield and tangible collateral, absorbed an extraordinary volume of that displaced capital.

The result was yield compression on a scale with no modern precedent in European property markets. Prime real estate yields fell from 5% to 6% in 2012 toward 3-3.5% by 2021, with some markets and sectors pushing below 3%. This was not driven by improving occupancy, accelerating rent growth, or better operating fundamentals. It was driven by a policy environment that made every competing asset class unattractive. Capital flooded in because there was nowhere else to put it, and prices rose accordingly.

For as long as that environment persisted, the returns it generated looked like real estate skill. They were not. The majority of total returns from European direct real estate during this period came from yield compression rather than income growth: the mechanical effect of falling discount rates applied to any income stream, in every sector, across every market simultaneously. A well-run logistics platform and a poorly managed retail centre both benefited, in proportion to their income. The tailwind was indiscriminate.

That era closed in July 2022, when the ECB began the sharpest tightening cycle since the euro was introduced. Within fourteen months, the deposit rate had moved from -0.5% to 4%. Assets priced on the assumption of near-zero rates for the foreseeable future had to reprice. They did. What is sometimes described as a collapse in European real estate values was, more precisely, a correction toward pricing that reflected the actual cost of capital.

The Structural Case Against Rates Returning to Previous Lows

The cyclical story of European rates is well understood: the ECB tightened aggressively, inflation retreated, and the deposit rate has since been cut back to 2%, where it has held through early 2026 as policymakers navigate persistent uncertainty. The structural story receives far less attention, which is the one that matters for long-term capital allocation.

Central banks do not determine the long-run equilibrium real interest rate. They track it. That rate, which economists call r-star or the natural rate, is set by forces well outside the ECB’s control: the global balance between savings and investment demand, demographics, productivity, and the fiscal stance of governments. For four decades before the pandemic, r-star in advanced economies declined persistently. Ageing European populations saved more and spent less. Weak investment demand across the continent absorbed little of that saving. Asian economies, running large current account surpluses, recycled capital into Western government bonds at scale, pushing yields lower across the board. The ECB was not choosing low rates as a policy preference. It was following a structural equilibrium that left it with no other option if it wanted to sustain growth and reach its inflation target.

Since the pandemic, that equilibrium has shifted. European governments have expanded fiscal deficits sharply and durably, absorbing private savings that previously flowed into sovereign bonds and bid down yields. NATO commitments are driving defence spending higher across the continent, with Germany alone reversing decades of fiscal conservatism. The energy transition requires private and public investment on a scale that competes directly for the same capital that once suppressed European risk-free rates. Research from the ECB and the San Francisco Federal Reserve now points to r-star in the euro area rising since the pandemic, with projections suggesting it will not return to pre-pandemic lows. The United States shows a parallel pattern, but the European dynamic is specific: fiscal expansion, defence investment, and energy transition capital requirements are not temporary. They are structural and sustained.

For real estate, the implication is precise. Assets priced in 2020 or 2021 were priced for a world in which the equilibrium real rate was close to zero and sovereign bonds offered nothing. That world has gone. Corrected values are not waiting to recover to previous levels. They reflect a new and more durable equilibrium. Allocators who understand this are not waiting for the old prices to return. They are assessing whether current prices, set against a structurally higher but now stable cost of capital, offer compelling forward returns on their own terms.

Operational Real Estate Is Being Paid for Again

Among the less-discussed consequences of a decade of yield compression was what it did to the pricing of operational complexity. When passive long-leased assets compressed to yields of 3-3.5%, operationally intensive real estate (logistics platforms, senior living, residential-for-rent, hotels, purpose built student accommodation and self storage) might yield 4.5-5.5%. The narrow spread between the two represented the entire compensation for management intensity, sector expertise, execution risk, and illiquidity. Against a risk-free rate near zero, that spread existed in relative terms. In absolute terms, investors were accepting very significant additional operational risk for limited incremental return.

By 2026 that has changed. With the ECB deposit rate at 2% and core European government bonds yielding 2.5-3%, well-positioned operational real estate in structurally undersupplied sectors yields 5-6.5%. The absolute compensation for accepting operational risk and illiquidity has widened in a way that has not been adequately priced into how allocators are thinking about the opportunity. The spread between passive income assets and genuinely operational ones has restored itself, and the investor who demands that differentiation now is operating in a market that prices it correctly, rather than one that collapsed the distinction because capital had nowhere else to go.

This matters most where operational skill genuinely drives outcomes. During the low-rate decade, even poorly run assets generated acceptable returns because yield compression lifted valuations across the board. That cover has gone. The difference between an operator who manages pricing dynamically, controls costs with discipline, and invests intelligently in the quality of the income stream versus one who does not is now reflected in actual returns rather than obscured by a market-wide tailwind. For investors with access to genuine operational capability, this is a more favourable environment. For those who relied on financial conditions to carry them, it is a harder one.

Not All Income Is Underwritten by the Same Thing

Real estate encompasses assets whose fundamental demand drivers are as different from each other as equities and bonds. At one end sit assets whose income depends on financial and economic conditions: city centre offices that fill and empty with corporate hiring cycles, development-stage assets whose viability turns on the cost of debt, retail parks whose footfall tracks consumer confidence. These assets are tightly connected to the economic and monetary cycle, and their repricing in 2022 to 2024 was rational.

At the other end sit assets whose demand is driven not by financial conditions but by demographics and social structure. Residential property in supply-constrained cities. Senior living and healthcare real estate serving an ageing European population. Purpose-built accommodation for students, workers, and urban renters whose need for housing does not diminish when the ECB raises rates. Last-mile logistics and self storage serving urban populations whose shift toward online consumption is structural, not cyclical. Each of these is, at its core, a response to a feature of European society that interest rate policy does not alter.

This distinction matters for how an investor should think about income security across a ten-year hold. Long-leased office income is contractually fixed but operationally exposed to a tenant who, at renewal, may take less space or leave entirely if their business has contracted. Residential or care facility income in a demographically constrained market is not contractually long but is underwritten by demand that does not recede with the rate cycle. The nature of the income security is different. In several respects, for a holder with a genuine long-term horizon, the demographic anchor is the more reliable of the two.

The rate cycle has sharpened this distinction rather than blurred it. Across Europe, sectors with structural demographic demand maintained occupancy and real income growth through the correction even as valuations adjusted to higher discount rates. The income did not deteriorate. Only the yield applied to it changed. That is a fundamentally different risk event from a sector where occupancy fell because the underlying demand driver is itself rate-sensitive. Conflating the two, which the low-rate decade made easy, produced the mispricing that is only now being unwound.

The Illiquidity Premium: Compressed for a Decade, Available Again

Private real estate is illiquid. Positions cannot be adjusted quickly, exit timing is partly outside the investor’s control, and capital calls must be met regardless of what listed markets are doing. The conventional economic argument is that investors should be compensated for accepting this through higher expected returns than equivalent liquid assets offer. For most of the past decade, that premium was not available. As institutional capital flooded into private real estate in search of any positive yield, competition for assets drove bid prices up and compressed spreads over listed equivalents to levels that did not compensate adequately for the illiquidity being accepted.

The correction changed this. Transaction volumes in European direct real estate fell sharply from 2022, bid-ask spreads widened, and buyers who remained active could negotiate on terms that reflected genuine illiquidity and execution risk. For investors deploying equity into corrected assets in sectors with structural income growth, the entry yield, the income growth potential, and the restoration of the illiquidity premium now combine to produce a forward total return case that is, on most reasonable assumptions, more compelling than anything available during the preceding decade. This is not a universal statement about European real estate. Offices in structurally impaired markets, development-stage assets with uncertain debt markets, and assets acquired at peak pricing with overlevered structures are in a different position entirely. Selectivity matters more now than it has for twenty years.

Stop Waiting for the Old Market to Come Back

European real estate has not underperformed. Assets priced on the assumption of indefinitely cheap money and a structurally low equilibrium rate have corrected to reflect a world in which neither of those conditions holds. That is not underperformance. It is a repricing, and it was rational. The pain was real, but it was concentrated where it belonged: assets that were overpriced, overlevered, or reliant on financial conditions to do the work that income fundamentals should have done.

What happens next is not a function of whether the ECB cuts by another 25 or 50 basis points. It is a function of whether the income fundamentals of specific assets, in specific sectors, justify the prices at which they can now be acquired. In sectors where structural demand was never impaired, where operational quality drives genuine income growth above inflation, and where supply constraints are physical and regulatory rather than financial, the investment case does not depend on a return to 2019 conditions. It stands without that crutch.

The investors waiting on the sidelines for European real estate to recover are, in most cases, waiting for the wrong matter. Recovery to prior valuations would require a return to prior rate conditions, and those conditions are not coming back. The productive question is not when the market recovers. It is whether specific assets, at current prices, with durable income backed by structural demand, offer returns that justify the illiquidity and the execution risk. In a growing number of cases, they do. That window will not stay open indefinitely.

Crosswind Capital Fund Management Limited is registered in the Abu Dhabi Global Market and regulated by the Financial Services Regulatory Authority (FSP: 220171). This article is for informational purposes only and does not constitute investment advice or a solicitation to invest.